Playing Monopoly in a climate crisis

How many people in New Zealand play Monopoly? I don’t mean the game. I mean literally in real life, in the socioeconomic climate.

Buying property, selling property. Leverage. Speculate. Invest. I count myself as one of them, although it was rather by accident.

Why am I talking about property, you ask? The planet is burning and no one cares! Believe me, I know. But give me a few minutes to build my case about how property can get more people to care.

It’s not the game of Life, but many believe it is.

But before I do, just this disclaimer: Though I consider myself an environmentalist and a social entrepreneur, I am also an investor.

I recognise that money often drives action in the world. I want to use my experience to inform others.

Our world needs real ideas and real change in order to survive. We need them now. Solutions in food, waste, transport, packaging, energy, and how to prevent countries from each electing their own version of Dr Evil.

We also need to steer people toward existing solutions like conservation, planting trees, fairness, and better economic models than ‘growth at all costs’ (Referencing donut economics or degrowth models). We need to apply resources toward these areas. Yesterday. Yesteryear. Yesterdecade.

Desperate times call

I am proposing to use property to fund our way out of this social and climate crisis. Because our side is losing ground. We land on a huge fine every round, and $200 passing ‘GO’ is not enough to sustain us in what feels like a rigged game.

So can we actively play a property game? Should we? Potentially.

My climate agency Popcorn Innovation is not funded. It is bootstrapped. I often work with fledgling pre-revenue businesses who can’t afford much of anything let alone a consultant. How I even afford to do this work, is by the virtue of my sporadic consulting income (plus my husband’s), and in equal measure, good property investments.

But, if more people used their property gains for change, perhaps we would have more funding available, more sustainable businesses, and more support for communities and people who are struggling..which is kind of what we need right now. And because if we get more investors to care, we can get more meaningful solutions out there.

Property investment vs climate investment

Have you heard that old adage, that 1 in every 10 businesses succeed?

Well, if an investor puts $1 million into 10 businesses and only 10% of them make it to decent profitability then potentially a 10% ‘Return on investment’, or ROI, might be achieved. As I understand it, this is the metric that investment funds are measured against. Some do better, some do worse. But that’s the goal.

Property growth in New Zealand is comparable to this figure. And it is arguably less risky.

Furthermore, you don’t even have to use all your own money! The banks often let you lend the majority of the cost, say ~80%..(with lots of interest of course), but it still often works to your advantage.

Which is why so much of the excess capital here does exactly that, going into real estate instead of into business and other investments.

This maybe the reason why raising money in this country isn’t easy. Why such a wealthy country per capita struggles to pay their nurses and teachers enough. Why it tends to under-invest in its own businesses and infrastructure. That and the forever touted Ponzi scheme of top-down economics, and political decisions that defund the government sector in the interests of privatisation by corporations and the wealthy.

Reverse division

Conversely, if you don’t own a home here, you will find it hard to start a business, or even buy a car. Property owners can loan from their mortgage at 5–7% interest rates. The financial mechanisms here aren’t like in international markets with 0% APR credit card offerings. Business loans and credit cards are more commonly at 15% APR and above.

How is someone who doesn’t own a home supposed to get ahead? Referencing rising rents, inflation, stagnant wages…the split paths of the have’s and the have nots. The answer, is simply that they don’t.

Without mum and dad

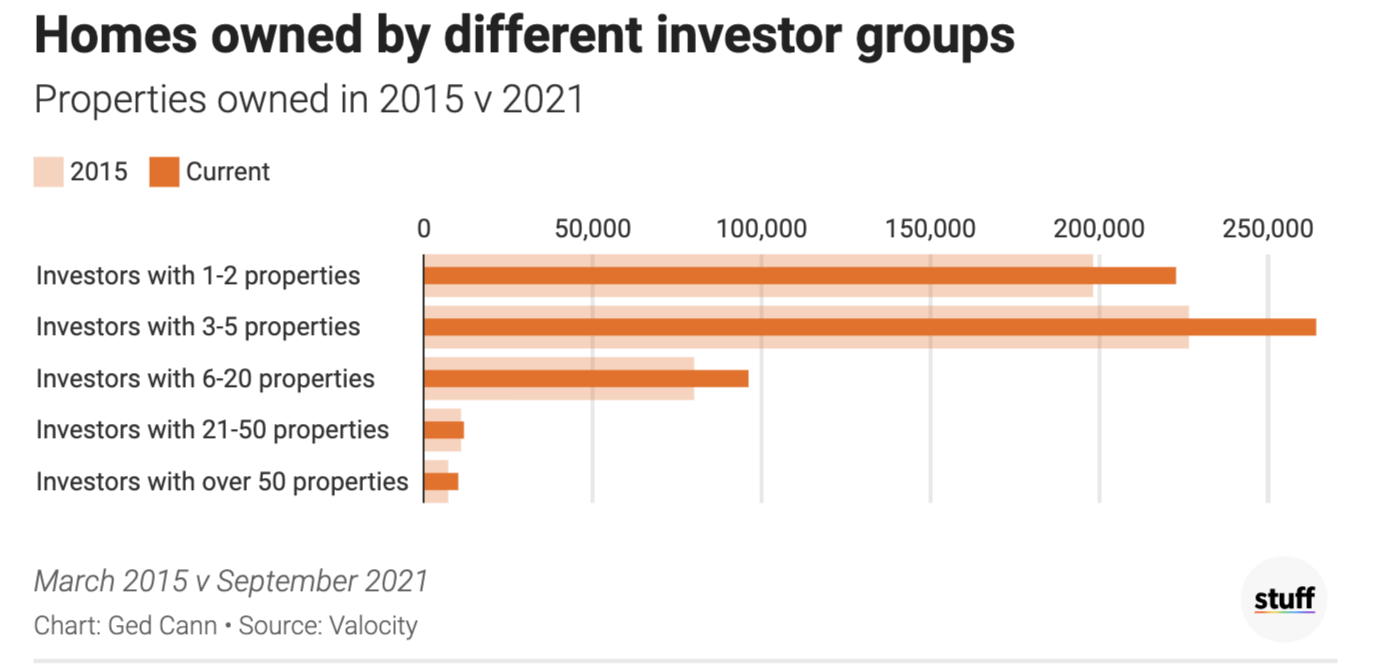

According to this article in Stuff about mega-landlords, 20 per cent of investor stock – or over 118,000 homes – are owned by people with six or more properties.

How does one get 6 or more properties? Well, they might have bought a long time ago, or they might be professional investors, or they might be part of a multi-generational family trust.

What if you aren’t part of the wealthy landowner club? You can work work work but saving will take a while before you can afford to buy.

And ownership by mum and pop investors is around 1/3 of housing stock, according to this NZ Herald article.

A lot of young people are currently locked out of the market by high pricing, and big land grabs are happening here and overseas by big investment firms and rich countries. Land needs to be grabbed for nature and people, not corporations.

Team up

For all these reasons above, I propose more programs for investors and home owners to team up with social entrepreneurs, activists, and first home buyers, to get into an investment.

This can be achieved in part through a shared ownership model that we use at Popcorn for venture. I adapted this methodology to residential property.

If you are an owner, you are a potential investor.

Consider acting for the benefit of your children and the positive changes you could effect while doing it. For those socially minded, consider that if you are in a position of strength, your ability to champion your causes also get stronger.

Money can be used for good.

Property isn’t doom

Most people are renting. Many are opposed to property investment, perhaps due to feeling it’s responsible for sky high prices and negligent landlords and the mega-investors that haunt these shores. Fair enough.

These will exist until we mandate and vote for a government that drives them away.

That being said, I actually find property investment is a sustainable endeavour in some ways.

A house is a building that should last decades, if not generations. We own a house from the 1940s. That’s almost three quarters of a century, and I expect it to last another half century if all goes well. Few products last that long these days.

It could use some more energy efficient heating and solar, but its existence isn’t wasteful. It provides shelter for people to live and sleep, its a place to work from home and store things, and a space for friends and family to gather.

The shared model can be deployed for people to buy larger land parcels which are shared among family, or friends with tiny homes. They might want to plant trees like my friends in Taupaki, or have a shared orchard like one group in Waiheke.

A means to an end

It’s not all roses, its often stressful, hard work, time consuming, and may distract you from your other priorities and goals. It is complicated buying with others, which is why most of the time it’s mostly close partners or families that do it. And just like business, it matters who you invest with, and your alignment with them both financially and philosophically.

But once you have it agreed and settled, it can be transformational. Property is, of itself, an enabler of life and security for the future. As an asset, property can be sold in whole (or in part). It can be also be loaned, hired, rented, improved, leveraged and traded.

The banks will lend money for it under the right conditions. And you can own property and do good with it.

I believe it’s a way to fund important work, and improve the lives of people. And if applied correctly, it can fill the gaps in our investment market towards climate, small business, and community projects.

And even if this weren’t the case, it’s a way to help those who are generationally disadvantaged, climate and social activists, and first home buyers.

It is not my intent to flood the market, so would aim information toward those that require it for these purposes.

If you’d like to know more about this topic, let me know by expressing interest here: or email me at popcorn.innovators@gmail.com.

*Note, however, that this still carries risk. Although property tends to go up in the long term, it is not guaranteed. Had we invested three years ago, this would not be the case today (property prices went down). So in this instance, an investor may not get the gains expected.

I am not a qualified financial advisor. These are my opinions, please seek your own advice before investing.